Economists' expectations for a slowdown in the United States economy were more than confirmed on Friday when the Commerce Department reported that real gross domestic product in the third quarter grew at the slowest rate since the beginning of the bull market in equities. This will inevitably affect the earnings outlook for companies, but at the same time, investors may be able to take heart from falling inflation and interest rates.

Third quarter US real GDP grew at an annualised rate of just 1.6 percent in the third quarter, well below Wall Street forecasts for a 2.2 percent growth rate. The third quarter's growth rate was down from 2.6 percent in the second quarter and the lowest since the first quarter of 2003.

The growth rate was negatively affected by a 17.4 percent annualised rate of decrease in residential investment. This confirmed economists' expectations that the weakening housing market would become a drag on the economy.

Predictably, bonds rose on Friday on the news, while the prospect for lower interest rates was apparently not enough to offset earnings fears as stocks fell.

Despite the sharp drop in the growth rate, there is still reason to think that the US economy will avoid sinking into recession. For one, the GDP report showed that consumer spending held up in the third quarter as personal consumption expenditures grew at a 3.1 percent rate, up from 2.6 percent in the second quarter. In addition, Friday also saw the final October reading of the University of Michigan's consumer sentiment index coming out at 93.6, up from a preliminary 92.3 and September's final reading of 85.4.

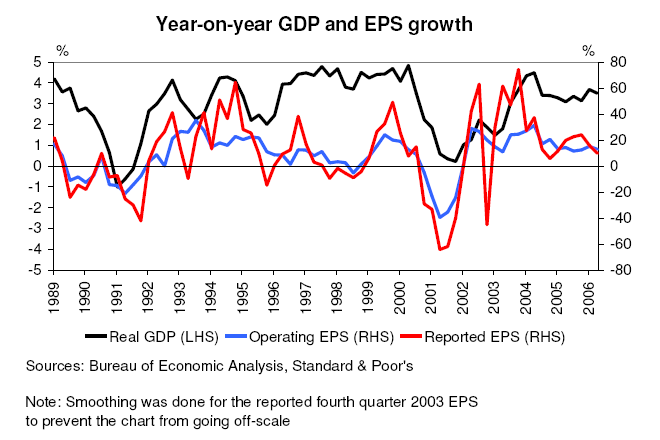

Other reports over the past fortnight indicated that the housing market has stopped weakening recently, with housing starts and new home sales increasing in September and homebuilder sentiment edging up in October, while in the manufacturing sector, new orders for durable goods rose a strong 7.8 percent in September, reversing previous months' declines. Adding to evidence that the economy could be stabilising is the Conference Board's Index of Leading Economic Indicators, which gained 0.1 percent in September. Nevertheless, investors should be aware that even if the economy stabilises at a low growth rate and avoids a recession, corporate earnings could still deteriorate significantly. Note, for examples, that in the following chart, even during the soft landing of 1995 and the no-landing of 1998, reported year-on-year earnings-per-share growth actually dipped into negative territory.

Nevertheless, investors should be aware that even if the economy stabilises at a low growth rate and avoids a recession, corporate earnings could still deteriorate significantly. Note, for examples, that in the following chart, even during the soft landing of 1995 and the no-landing of 1998, reported year-on-year earnings-per-share growth actually dipped into negative territory.

What ultimately supported the stock market in 1995 and 1998 were falling interest rates. In both years, the Federal Reserve cut interest rates.

In this regard, the GDP report is encouraging in that it showed that the rate of appreciation of the price index based on personal consumption expenditures decelerated in the third quarter, slowing to a 2.5 percent annualised rate from 4.0 percent in the second quarter for the overall index and to a 2.3 percent rate from 2.7 percent for the core index that excludes food and energy.

So if the US economy does stabilise around the current growth rate -- admittedly a big "if" -- while the inflation rate continues to decline, the net effect could -- apart from possibly some volatility -- actually be quite benign for equity investors.

It would not exactly be the Goldilocks scenario that optimists often tout, but it would not be the stagflation that pessimists fear either.

1 comment:

4QR GDP growth will most likely be lower. The housing ongoing collapse should result in lower HEW's and lost jobs in the residential housing sector (construction, marketing, financing, etc.). The glut of unsold cars, trucks and SUV's will also contribute. Finally, change in Fed funds rates impact the economy with a delay of about 9 months. So we still haven't seen the effect of the full 5.25% rate.

A worsening of the trade gap, if it happens, would also reduce GDP growth. Partially offsetting these variables, higher consumer spending due to Christmas shopping would help GDP growth. However, given the current indebtedness and higher credit card interest rates, I expect Christmas shopping to be lower than in the previous couple of years.

Ernst

Post a Comment