There were good news and bad news for the US economy yesterday. Reuters reports that consumer spending slipped in August.

[T]he U.S. Commerce Department said that...inflation-adjusted spending in August fell surprisingly by 0.1 percent, the first decline since a 0.3 percent drop in September 2005...

Wage and salary income edged up 0.1 percent. The personal saving rate improved to a negative 0.5 percent, but it was nevertheless the 17th consecutive negative reading in that category.

Inflation did not help.

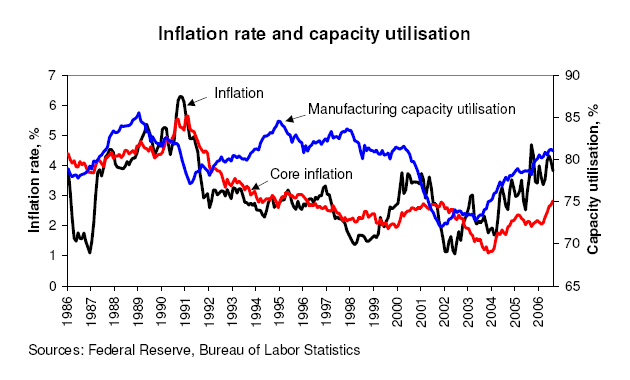

The Commerce Department said core U.S. consumer prices rose 0.2 percent in August, as expected. But the year-on-year rate of nonfood, nonenergy inflation rose to 2.5 percent, the highest since April 1995, and well above the 1 percent to 2 percent seen as a "comfort zone" by some Federal Reserve officials.

But there is hope for improvement.

The University of Michigan's closely watched consumer sentiment index rose to 85.4 in September, up from 82.0 in August and the highest since April...

Anecdotally, Americans sense that inflation is coming down, if slowly. The Michigan survey's forecast of five-year inflation fell to 3.0 percent in September from August's 3.2 percent.

And the industrial sector may be in better shape than earlier thought.

A key indicator of business conditions in the U.S. Midwest, the National Association of Purchasing Managers-Chicago index jumped unexpectedly to 62.1 in September from 57.1, beating out even the most optimistic forecasts. Economists, on net, had expected a small decline.

But even here, the news is mixed.

Still, the purchasing managers' index from the neighboring Milwaukee, Wisconsin, area slumped to 56 points from 62 in August as new orders and production fell.

Common to both regions was a decline in the employment indices, suggesting companies are becoming less willing to hire new staff. Measures of "prices paid" were also down on the month -- as expected, given the trend in energy prices.

The news from Europe yesterday was also mixed.

Bloomberg reports rising confidence and lower inflation in the euro zone in September.

An index of sentiment among executives and consumers in the dozen nations sharing the euro rose to 109.3, the highest since February 2001, from a revised 108.3 in August, the European Commission said today in Brussels. Inflation slowed to 1.8 percent in September, dropping below the ECB's 2 percent limit for the first time since January 2005, a separate report showed.

But German retail sales disappointed.

... German retail sales unexpectedly stagnated in August on concern that the higher sales tax will contribute to slower growth next year, the Federal Statistics Office said today.

Reuters also reports some weakness in the UK.

The Bank of England said credit card lending fell 311 million pounds in August, its biggest fall since records began in 1993...

Broader consumer credit rose by 755 million pounds last month, missing forecasts for a 900 million pound rise and July's 1 billion pound increase.

Mortgage lending rose by 9.1 billion pounds in August, less than the 10 billion forecast and down from 9.3 billion in July, while approvals for home loans came in slightly lower than expected at 119,000 in August.

But again confidence seems to be improving.

GfK NOP's consumer confidence index rose to -7 from -8 in August when people's mood took a hit after the shock rate rise and a security alert at London's Heathrow airport which stranded thousands of holidaymakers.

Of course, whatever happens in the developed economies, they will not be able to match India's growth rate. From AFP/CNA:

India, the world's second-fastest growing economy after China, has reported an 8.9 percent expansion in the first quarter to June, beating most forecasts, official data shows.