This Wednesday, the Federal Open Market Committee will decide whether to raise interest rates. The consensus view is that it will not, especially after the latest US inflation figures. However, at least one measure of resource utilisation indicates that some inflationary pressure persists and further rate hikes down the road cannot be written off.

On Friday, the US Labor Department reported that consumer prices, both overall as well as core prices (excluding food and energy), rose 0.2 percent in August. This is a slower pace than in previous months, and suggests that inflation in the US has passed or is at least nearing a peak.

Signs of a slowing economy reinforce this impression. Friday also saw the Federal Reserve report that industrial production declined 0.1 percent in August compared to an increase of 0.4 percent in July. Industrial capacity utilisation slipped to 82.4 percent in August from 82.7 in July while manufacturing capacity utilisation slipped to 81.0 in August from 81.2 in July. Rising capacity utilisation over the past few years had been a source of inflationary pressure.

However, not all data are showing lower inflationary pressure. Another report from the Labor Department on Thursday showed that US import prices rose by 0.8 percent in August while nonpetroleum import prices climbed 0.5 percent. Even prices for imports from China were up -- for a second consecutive month -- albeit by a slight 0.1 percent.

Even where the data indicate a slowing economy, the question remains whether it is slowing fast enough to make an appreciable dent on inflation in the near future. For example, Thursday also saw the Commerce Department report that US retail sales rose 0.2 percent in August. While this shows that consumer spending is slowing, underlying consumer demand may still be relatively strong, as retail sales excluding autos and gas actually rose 0.4 percent.

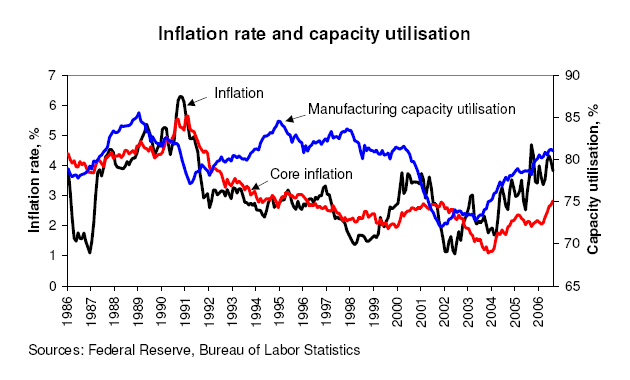

Let us take another look at the capacity utilisation data and relate them to inflation. The accompanying chart shows that historically, the annual rate of consumer price inflation -- for both headline and core -- follows manufacturing capacity utilisation. It does so with a lag -- a considerable lag in fact, especially for core inflation.

The accompanying chart shows that historically, the annual rate of consumer price inflation -- for both headline and core -- follows manufacturing capacity utilisation. It does so with a lag -- a considerable lag in fact, especially for core inflation.

The chart also shows that, despite the recent drop, from a longer-term perspective, a peak in capacity utilisation is hardly discernible at the moment, and the manufacturing capacity utilisation of 81.2 percent is already above its 1972-2005 average of 79.8 percent.

So if the chart is any indication, inflation is likely to persist around current levels for quite a while longer.

If that turns out to be the case, how would the markets, economists, and most importantly of all, the Federal Reserve react? We can try to guess, but at least we already have an idea of what the International Monetary Fund thinks the Federal Reserve should do. Its recent World Economic Outlook report had this to say about inflation in the US:

Despite the recent slowing in growth, inflationary pressures have begun to edge up as excess capacity in product and labor markets has diminished (and actually been eliminated on some measures), energy prices have risen and begun to feed through into some other prices (particularly transportation), and the restraining effect that globalization has had on inflation in recent years has faded.

Then, after noting the pause in the Federal Reserve's rate hiking campaign in August, it added that "given the importance of keeping inflation expectations firmly in check, some further policy tightening may still be needed".

Let us see whether the Federal Reserve agrees.

No comments:

Post a Comment