US second quarter GDP growth has been revised up. Reuters reports:

The U.S. economy grew at a 2.9 percent annual pace in the second quarter, faster than the 2.5 percent rate initially reported but marginally below what analysts were expecting, as higher business investment offset a drop in residential construction, a Commerce Department report showed.

At the same time, an inflation gauge favored by the Federal Reserve -- which measures personal consumption expenditure prices minus food and energy -- was revised to 2.8 percent, the biggest rise since the first quarter of 2001. The inflation index originally was reported to have risen by 2.9 percent when figures were released last month...

Corporate profits after taxes rose 2.1 percent in the second quarter, well below the 14.8 percent rise in the first three months of the year.

Other economic data released yesterday:

A separate report by the ADP Employer Services showed private-sector employers added 107,00 new jobs in August. The data comes two days before the government's nonfarm payrolls report, which are expected to show 120,000 new jobs in the month...

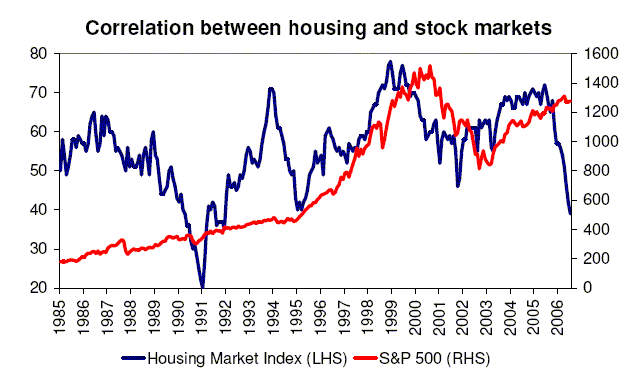

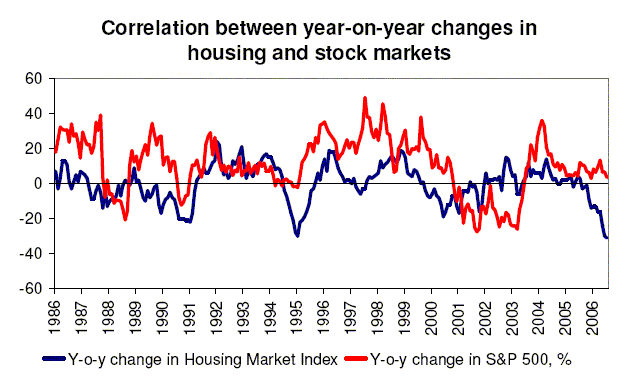

Also, U.S. mortgage applications fell for the first time in four weeks as demand for home purchase loans dropped to the lowest level in nearly three years, a report from the Mortgage Bankers Association said.

Fed officials are apparently not worried about the slowdown, according to another Reuters story:

The U.S. economy can weather a slowdown in the housing sector as rising incomes and business investment offer support, Federal Reserve officials said on Wednesday as they pointed to inflation risks.

"Rising disposable incomes should enable household spending to expand at a moderate pace and provide continued support for the overall economic expansion," Federal Reserve Chairman Ben Bernanke said in a letter to a lawmaker released on Wednesday...

Dallas Federal Reserve Bank President Richard Fisher said the economy could be rotating away from reliance on household spending to investment, setting a stage for healthier growth.

Richmond Fed chief Jeffrey Lacker -- who dissented from the central bank's August 8 decision to hold borrowing costs steady -- said there were few signs the housing slowdown was eating into household net worth or overall construction employment.

Lacker told Bloomberg Television he remained concerned on the inflation front and said his outlook had not shifted since the Fed's meeting, despite a softer inflation report and a slew of data indicating a sharp housing correction.

Perhaps Lacker has the UK experience in mind, where the central bank apparently ended its tightening campaign too soon, and is now seeing the largest rise in rents since 1988, London becoming the world's most expensive residential market, and mortgage lending growing in July by its biggest amount since 2003 and retail sales rising swiftly in August.

Sweden's Riksbank certainly sees the need for higher rates, raising its repo rate yesterday by a quarter point to 2.5 percent, its fourth hike this year.

China, which has revised its 2005 economic growth figure upwards to 10.2 percent from 9.9 percent, did not raise interest rates yesterday, but it did announce a one percentage point hike in the required reserve ratio for foreign currency deposits for banks, even as the exchange rate of the renminbi against the US dollar hit a new high yesterday.

One country that is seeing unexpected slowing is Japan. Reuters reports that retail sales fell in July.

Heavy rain and surging energy costs kept Japanese shoppers at home in July, sending retail sales slumping 1.7 percent from the previous month.

Compared with a year earlier, retail sales fell 0.2 percent, short of economists' median forecast of a 0.3 percent rise, data from the Ministry of Economy, Trade and Industry showed on Wednesday...

Other government data on Wednesday showed Japanese salaried workers' total cash earnings fell slightly in July from a year earlier, the first decline in six months...

Average overtime pay, seen by some economists as a better barometer of income conditions, rose 1.5 percent in July from a year earlier, the 48th straight monthly increase.

The data also showed the number of full-time employees rose 1.6 percent year-on-year, while the number of part-time workers fell 0.6 percent -- possibly a sign that companies were willing to pay more for skilled workers.

And today, we get another Reuters report saying that Japan's NTC Research/Nomura/JMMA Purchasing Managers Index fell to 54.6 in August from 55.7 in July, which appears consistent with another report today from Bloomberg saying that Japan's industrial production fell 0.9 percent in July.